How the Migration of Skilled Workers to the Gig Economy Is Threatening Apparel Exports

By Perfect Sourcing Research Desk

For years, the Indian apparel industry believed its biggest challenge was winning orders from global brands.

Today, a far more serious challenge is emerging.

The orders are arriving.

The workers are not.

Across India’s major apparel manufacturing hubs, a growing number of skilled garment workers are leaving factory floors and joining food delivery platforms, quick-commerce companies, logistics operators and warehouse networks. What began as a post-pandemic labour disruption has evolved into a structural workforce shift with significant implications for India’s manufacturing competitiveness.

The issue has become particularly concerning at a time when India is attempting to capitalize on global sourcing diversification, free trade agreements and the China+1 strategy.

Industry leaders now warn that labour availability—not order availability—could become the single biggest constraint to growth.

The Numbers Behind the Crisis

India’s textile and apparel sector employs nearly 45 million people directly and indirectly and contributes significantly to exports, manufacturing output and employment generation. Yet labour shortages are now being reported across almost every major apparel cluster.

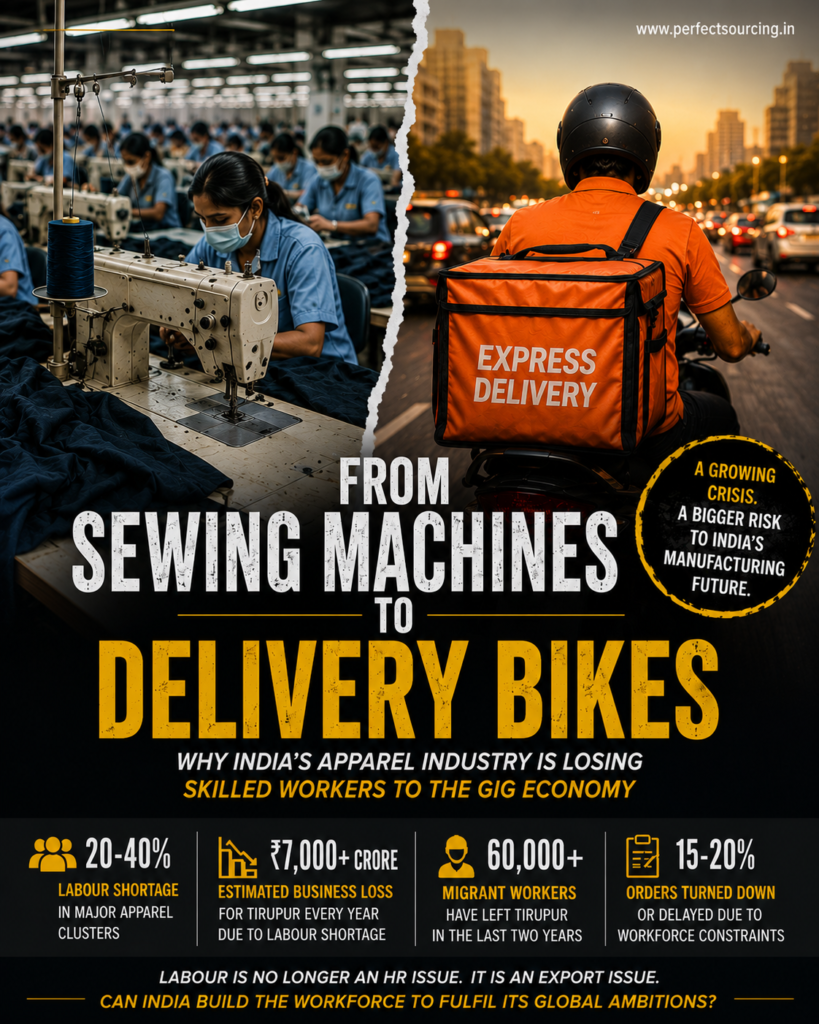

Tiruppur, India’s largest knitwear export hub, offers perhaps the clearest indication of the problem.

The ₹70,000-crore cluster, which accounts for approximately 90% of India’s cotton knitwear exports, has reported labour shortages ranging from 20% to 40% over the last two years. Industry reports indicate that 60,000 migrant workers have already exited the cluster, while previous estimates suggested a shortage of 100,000-150,000 workers during peak periods.

According to exporters, some factories are currently operating with nearly 40% fewer workers than required.

This is no longer a temporary labour gap. It is becoming a structural shortage.

Why Factories Are Losing Workers

Conventional wisdom suggests workers leave for higher wages.

The data suggests a more complex reality.

A skilled sewing operator in Tiruppur, Noida or Bengaluru typically earns between ₹18,000 and ₹25,000 per month including incentives.

A delivery executive working for food delivery or quick-commerce platforms can earn comparable amounts during peak periods.

The difference lies in flexibility.

Gig-economy jobs offer:

- Flexible working hours

- Weekly or faster payouts

- No fixed shifts

- No production targets

- Lower entry barriers

For younger workers entering the labour force, these factors are increasingly outweighing the perceived benefits of factory employment. The rapid expansion of India’s gig economy is expected to create millions of additional jobs over the coming years, intensifying competition for labour.

The Business Cost Is Much Larger Than Wage Inflation

Most discussions around labour shortages focus on rising wage bills.

In reality, wages are only a small part of the problem.

The bigger issue is lost productivity.

A sewing operator with five years of experience can often produce 30-40% more output than a newly hired worker.

When experienced workers leave, factories face:

- Lower line efficiency

- Increased defect rates

- Longer training cycles

- Higher overtime costs

- Shipment delays

Many exporters report that production lines require three to six months before replacement workers achieve expected productivity levels.

For export-oriented factories operating on tight margins and fixed delivery schedules, even small productivity declines can have significant financial consequences.

Tiruppur: A Case Study in Lost Opportunity

Tiruppur is perhaps the most telling example of how labour shortages can limit industrial growth.

The cluster generates approximately ₹70,000 crore in annual business and employs hundreds of thousands of workers. Yet labour shortages continue to constrain expansion plans.

Industry executives estimate that if labour shortages reduce effective production capacity by even 10%, the cluster could be foregoing business opportunities worth ₹7,000 crore annually.

If capacity constraints approach 15-20%, the economic impact becomes even larger.

This is not necessarily visible in export statistics.

It appears in orders that are never accepted, buyers who diversify sourcing, and expansion projects that never move forward.

The Impact on Other Major Clusters

Noida-Gurugram

The NCR garment belt faces direct competition from e-commerce, warehousing and quick-commerce companies.

Exporters report increasing recruitment costs, higher attrition rates and growing difficulty in retaining younger workers.

The challenge is particularly acute for entry-level operators and helpers.

Ludhiana

The hosiery cluster is witnessing shortages of machine operators and knitting specialists.

The impact becomes especially visible during winterwear production cycles when labour demand peaks.

Manufacturers increasingly rely on overtime and contract workers, reducing profitability.

Bengaluru

Karnataka’s apparel industry faces rising labour mobility as workers move between manufacturing, logistics and platform-based employment.

At the same time, higher transport and energy costs are adding further pressure on manufacturing economics.

Why This Matters for India’s Export Strategy

The timing could not be worse. Global buyers are actively diversifying sourcing away from China.

India is negotiating trade agreements. International retailers are seeking alternative manufacturing bases. Yet labour shortages threaten India’s ability to capitalize on these opportunities.

Industry observers note that workforce constraints are increasingly becoming a concern for buyers evaluating India’s long-term scalability.

The concern is simple:

Can India deliver significantly larger volumes if demand rises?

Without sufficient labour, the answer becomes uncertain.

The Long-Term Risk: Losing Competitive Advantage

Historically, India’s apparel industry competed on three strengths:

- Scale

- Skilled manpower

- Cost competitiveness

Labour shortages directly affect all three.

As labour becomes scarce:

- Productivity falls

- Costs increase

- Lead times extend

- Expansion slows

Meanwhile, competing sourcing destinations continue to invest aggressively in workforce development and manufacturing infrastructure.

The danger is not that India loses existing business. The danger is that India fails to capture future growth.

The Solution Cannot Be Higher Wages Alone

Most industry leaders agree that wage increases alone will not solve the problem.

The workforce entering manufacturing today has different expectations than previous generations.

Factories must compete not only on compensation but on overall employment experience.

What Needs to Change?

- Worker Housing Infrastructure

The majority of labour shortages in major clusters involve migrant workers.

Industry-led housing initiatives can improve retention and reduce migration volatility.

- Productivity-Linked Earnings

Highly skilled operators should have a clear pathway to significantly higher earnings.

Factories must reward productivity rather than tenure alone.

- Career Progression Frameworks

Many workers leave because they see no long-term career opportunities.

Structured growth pathways from operator to supervisor and management roles can improve retention.

- Flexible Workforce Models

The gig economy has demonstrated the value of flexibility.

Manufacturers may need to explore alternative shift structures and workforce models.

- Automation and Digitalization

Automation will not replace labour entirely, but it can reduce dependency on manual processes and improve productivity.

CLUSTER-WISE LABOUR GAP & ESTIMATED BUSINESS IMPACT

India’s Major Apparel Clusters Are Running Short of Workers

| Cluster | Estimated Annual Industry Turnover | Estimated Labour Gap | Estimated Capacity Impact | Potential Annual Business at Risk* |

| Tiruppur | ₹70,000 Cr | 20-40% | 10-15% | ₹7,000-10,500 Cr |

| Noida-NCR | ₹35,000-40,000 Cr | 15-25% | 8-12% | ₹2,800-4,800 Cr |

| Ludhiana | ₹30,000 Cr | 15-20% | 8-10% | ₹2,400-3,000 Cr |

| Bengaluru | ₹25,000 Cr | 15-20% | 7-10% | ₹1,750-2,500 Cr |

| Jaipur | ₹12,000-15,000 Cr | 10-15% | 5-8% | ₹600-1,200 Cr |

*Indicative industry estimates based on reported labour shortages, production disruptions, delayed orders, overtime costs and lost capacity expansion opportunities.

Combined Impact

Across these five major manufacturing clusters alone, labour shortages could be putting nearly ₹15,000-22,000 crore worth of annual business opportunities at risk.

The impact is not always visible in export statistics because much of the loss comes from:

- Orders not accepted

- Capacity expansions delayed

- Production inefficiencies

- Higher rejection rates

- Longer lead times

- Buyers diversifying sourcing destinations

Conclusion: India’s Next Competitive Battle Will Be for Talent

For nearly three decades, the Indian apparel industry has focused on building factories, increasing capacities, improving compliance standards and winning global buyers. Those efforts have paid off. Today, India is better positioned than ever to benefit from shifting global supply chains, growing geopolitical realignments and the search for alternatives to China.

Yet, a critical question remains unanswered.

Who will work in these factories?

The industry’s traditional assumption—that labour will always be available—can no longer be taken for granted. The emergence of the gig economy has fundamentally altered the employment landscape. For the first time, manufacturing is competing not just with other factories, but with technology platforms, logistics networks and a new generation of jobs that offer flexibility and independence.

This is why the labour shortage should not be viewed as a temporary disruption caused by migration patterns or wage pressures. It is a structural shift in workforce aspirations.

The challenge is particularly significant because India’s biggest opportunity lies ahead. However, scaling manufacturing without a scalable workforce is impossible.

History shows that countries become manufacturing leaders not simply because they have factories, but because they have a reliable ecosystem of skilled workers. Bangladesh built its apparel success on workforce availability. Vietnam invested heavily in skills and productivity. China combined manufacturing infrastructure with labour scale.

India’s next phase of growth will depend on whether it can create an equally compelling proposition for workers.

The solution will require a shift in mindset. The future workforce will not be attracted by wages alone. It will seek better working environments, career progression, housing, skill development, financial security and dignity of work. Companies that understand this transformation early will gain a significant competitive advantage.

The labour shortage confronting the industry today is, therefore, much more than an operational challenge. It is a test of India’s readiness to become a global manufacturing powerhouse.

The apparel industry has spent years asking how to attract more orders.

The more important question now may be: Can India build the workforce needed to fulfil them?

Because in the decade ahead, the factories that win global business will not necessarily be those with the newest machinery or the largest capacity. They will be the ones that succeed in attracting, developing and retaining talent.

And that may well determine whether India becomes the world’s next sourcing hub—or merely its next opportunity.